[по русский]

While foreign governments apply sanctions worldwide, Israeli banks continue to manage their perceived ‘sanctions risk’ by unfairly refusing services to Israelis who seek to transfer legitimate funds from abroad.

In other words: people who are not under sanctions are being treated like criminals in the Israeli banking system.

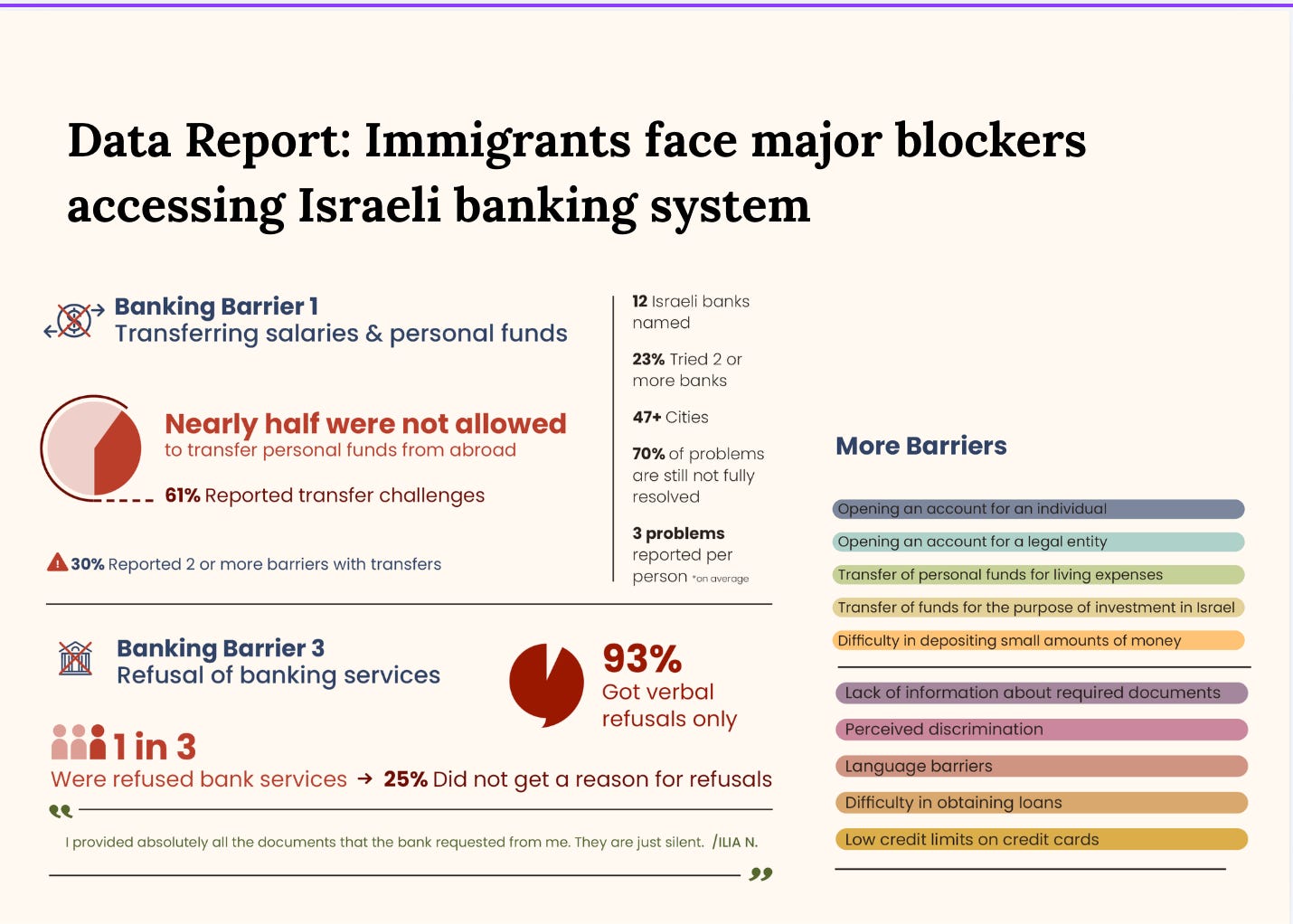

The Economic Integration Org has documented this since 2022, with thousands of cases sent to the Bank of Israel and lawmakers in the Israeli Parliament. We have also taken legal action in the Supreme Court against the major banks and the banking regulator to address this systemic flaw in Israel’s system.

Following our actions, in December 2025, the Bank of Israel published Directive 412 - here’s what it means for you.

Before you continue, please take a moment to respond to our 1-minute survey (an update that will help our 2026 legal action)

The full text of the new regulation pictured above, Directive 412 re: Proper Conduct of Banking Business, can be found here (BoI site). The text is in Hebrew, and is not yet available in English. The English portal to banking regulation is here.

The good news inside the new regulation:

According to Attorney Anna Moshe, who has led the legal action for the Economic Integration Organization since its founding,

In Section 4, The Bank of Israel recognizes the need to regulate how banks provide services to their customers at a time when foreign governments use sanctions worldwide.

In section 9, the Bank of Israel requires the banking corporations to develop professional expertise in the issue of sanctions.

In Section 11, with this regulation, the BoI reminds banks to issue any refusals in writing (something that was already a law, yet banks continue to refuse services verbally). The directive does not specify a timeline for a refusal in writing.

Anna Moshe testifies at Israeli Parliament December 8, 2025 Additionally, in a minor move that increases convenience to the customer, The Bank of Israel translated its actual complaint form to English on the government portal, not merely the landing page, as before.

Finally, senior Israeli lawmakers from across the political spectrum have taken an interest in this topic, starting with Oded Forer (Yisrael Beitenu) who began hosting us in multiple Immigration Committee meetings on the topic since 2023, as well as David Bitan (Likud) who hosted us at an Economic Affairs Committee discussion at the request of Oded Forer, as well as Avi Maoz (Noam), and Tatiana Mazarsky (Yesh-Atid), who have met with the regulator to get answers on this issue.

But the new regulation is not nearly enough. Here’s why:

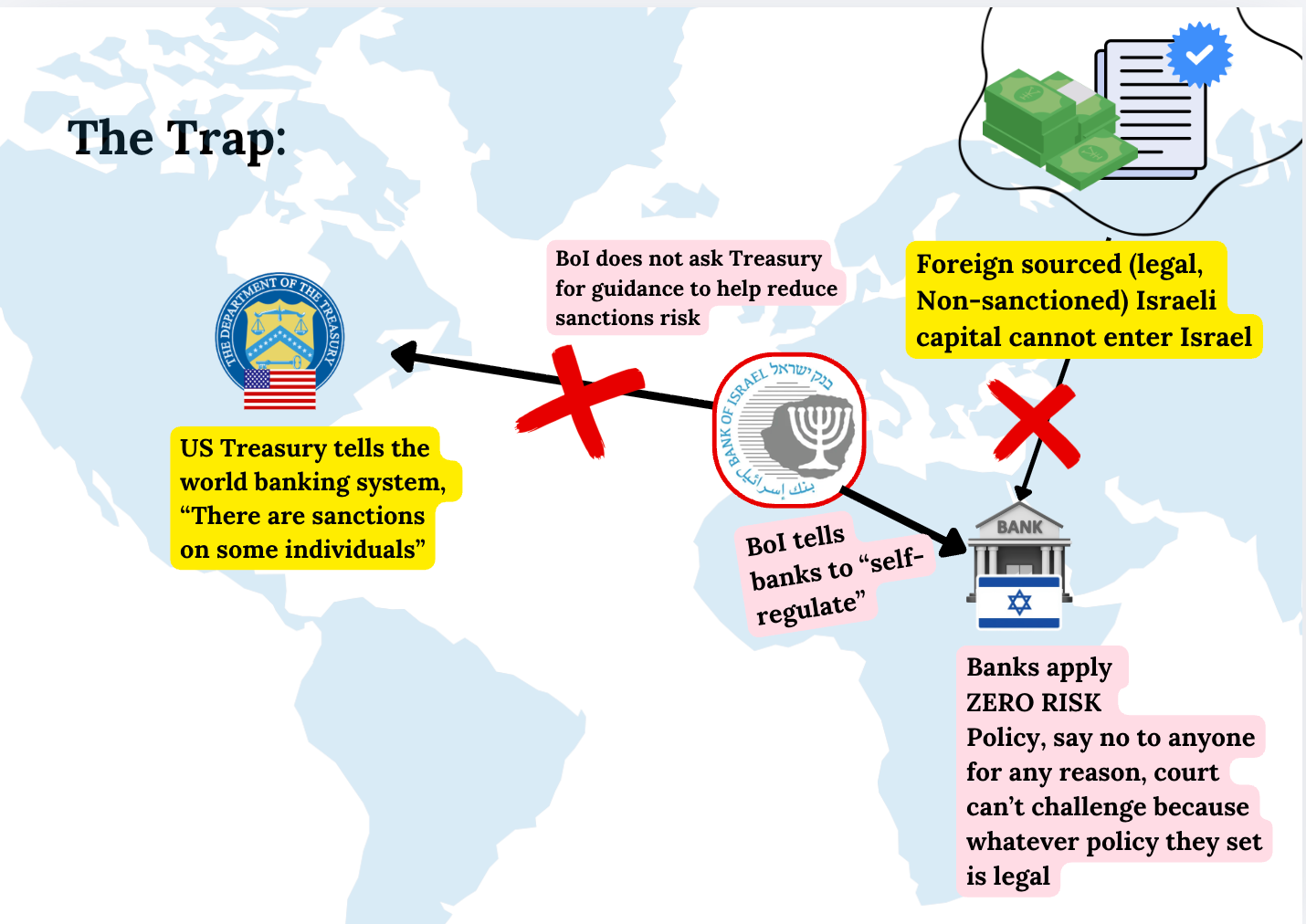

Today, the Bank of Israel allows banks to set their own policies and workflows, including, for how to approve foreign money for transfer into Israel. Under the regulation of the Bank of Israel, any refusals under a bank’s own policy are legitimate. This means an Israeli customer cannot take a bank to court for unfairly refusing them critical services.

Since Israeli banks take on all the perceived ‘sanctions’ risk of accepting foreign money transfers, they create their own workflows to accept foreign money - however they want, with no oversight.

What really happens: in a well-documented phenomenon, banks apply a policy of ‘zero risk’ and issue sweeping, blanket refusals to legitimate Israeli customers who have documentation to support the legitimacy of their funds. Many times, these refusals are verbal, with no documentation, nor opportunity to appeal a decision.

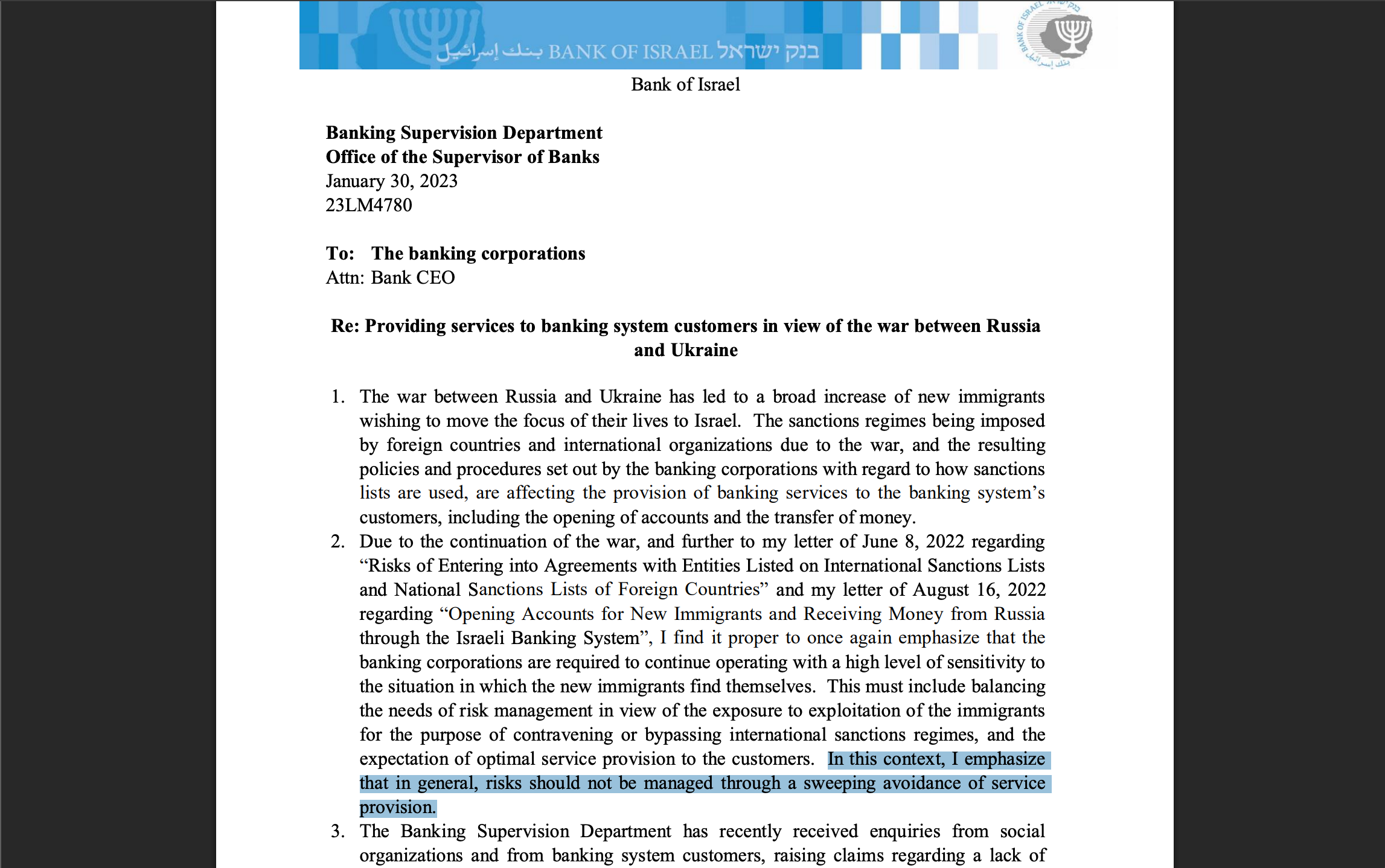

As a result of our community’s efforts in reporting data, the Bank of Israel first acknowledged that ‘blanket refusals’ are a problem in the January 30, 2023 letter they issued in response to our reporting. However, the directive they published was non-binding, and not enough for the banks to change their ways. That is why we petitioned Israel’s High Court of Justice last year.

The damage - immigrants can’t make their life in Israel, Israel’s economic sovereignty is harmed, and the state cannot receive hundreds of millions in foreign-sourced investment, which legally belongs to Israelis.

The directive directly infringes on Israel’s economic sovereignty, and allows foreign governments to interfere in Israelis’ basic access to the financial system (a critical utility like water or electricity).

It also deprives Israel of hundreds of millions in foreign investment which is currently stuck in correspondent accounts, unable to clear compliance and enter Israel.

What needs to be done:

In an ideal scenario, the government must take some of the risks off the banks, and in exchange, demand the banks follow clear risk-reduction workflows. This will benefit the state, the banks, and the customers.

In a more realistic scenario, the Bank of Israel must regulate the banks’ creation of customer-facing policies, and stop allowing the banks to make up their own rules, which allow them to deny services to anyone they want, for any reason and call it risk management.

In detail - what the end result should look like for the customer:

The Bank of Israel must regulate the banks and force them to provide a clear, uniform set of RULES that explain to bank customers and bank employees:

What is the initial list of documents for customers, required for transfers of funds in different situations, and other services;

What is the secondary list of documents that may be requested at the bank’s discretion connected to specific regulatory compliance;

Setting out timelines required by law for requests and responses;

A list of valid reasons for refusals of services;

An official appeals process for customers to correct errors or dispute refusals;

Guidelines for depositing relatively small amounts of cash up to $10,000 (the amount that can be brought across the border undeclared)

Banks must also make online banking interfaces fully available in English (including mobile apps).

A real consumer protection bureau.

Next steps by the Economic Integration Organization

We will continue to take legal action to achieve the stated goals of the Fair Banking Project. To help, please respond to our updated 1-minute survey here for 2026.

Thank you.

Contact information:

Sophia Tupolev

The Economic Integration Organization

+972-54-996-2486

sophia.tupolev@economic-inclusion.org